FORESTRY INDUSTRY MARKET AND PRODUCTION LINE INTELLIGENCE

b. Market size and coverage

EPTDA continually strives to develop relevant tools for its members, helping them stay competitive in a constantly evolving marketplace and business environment.

The purpose of this document is to provide distribution management and their sales forces with market and production line intelligence on the Forestry industry, primarily in the process from felling the tree to the manufacture of wooden planks, ready for the building industry and general carpentry. This document explores trends, identifies products used in the extraction of wood from forests, the transportation and laminating process; it clarifies key challenges, and considers the opportunities for distributors and how these can be capitalised, commercially.

This document has been divided into three parts:

OverviewPurposeof this document

2. Production Line Intelligence Pages 14-27

This section illustrates the extraction and processing of timber with a fully detailed production line schematic, so as to provide an understanding of what is involved and where the opportunities lie. Key customer challenges, major product groups, typical maintenance, and improvement projects are identified throughout the line, as well as highlighting potential areas of commercial opportunity for the distributor.

e. Overview of challenges Key producers

As part of the development of tools and resources for members, this document is designed to add value to their commercial understanding of specific markets and production line processes. This document, on the Forestry industry, follows reports on the Soft Drinks industry, Confectionery, the Automotive industry, Material Handling, Recycling and most recently, Aggregates.

This first section provides an introduction and overview to the Forestry industry and gives key background information, market intelligence, and major players within the industry. It has been organised as follows:

c. European sales data and evolution

d. Current and future market trends

a. Definition, segments within the industry, and market share

The opportunities within Forestry, both for MRO and OEM distribution, are significant – a minimum combined ‘scale of opportunity value’ (SOV) of 300m€ has been estimated as available for distribution of Power Transmission products in the sawmill aftermarket. The final section proposes how the document could be used and provides open-ended questions that can be asked of prospective customers in order to reinforce the knowledge gained in parts one and two and to maximise the available opportunities.

3. Use of this Document Pages 28-29

EPTDA was founded as the European Power Transmission Distributors Association in 1998 on the initiative of a group of power transmission and motion control (PT/MC) industrialists who believed in bringing together PT/MC distributors and manufacturers on one unique platform. It has since become the largest organisation of PT/MC distributors and manufacturers in EMEA and is one of the most powerful and respected B2B executive platforms for the industry worldwide.

1. Industry Overview Pages 4-13

EPTDA’s mission is to strengthen its members in the industrial distribution channel to be successful, profitable, and competitive in serving customers to the highest standards. The association takes great pride in its values which focus on being a premier community for qualified members through open dialogue and mutual respect; acting with integrity, honesty, and fairness; and ensuring continuous growth and learning.

3

f.

g. Major machine & system builders

Logging residues or primary forest residues

In 2019, it was estimated that there are around 420,000 enterprises operating in forest-based industries in Europe. This includes pulp and paper, furniture, printing and bioenergy sectors. Representing nearly a fifth of manufacturing enterprises in the EU, together they generated a combined turnover of more than 520bn€.3

Looking at the global forestry and logging market alone - it was estimated to be worth 475bn€ in 2020 and is forecast to reach a value of 644bn€ by 2025 at a CAGR of 6.3%.2

PART ONE Forestry Industry Overview

This market consists of the sales of forestry products and logs by organisations that produce, harvest and/or process them, and are involved in growing, cutting and transporting timber; operations

Forestry – defined as the management of trees and other vegetation in forests – is an important industry in Europe. Nearly 60% of wood harvested in Europe is then processed by European forest-based industries, accounting for around 7% of Europe's manufacturing GDP. However, contribution to Europe's total GDP is heavily influenced by region. Overall, the forest sector accounts for less than 1% of Europe's total GDP, but the Northern regional alone contributes over 40% of this.1

Forestry materials are usually collected as:

Processing residues or secondary forest residues

of the timber tract; growing trees for reforestation; and collecting forest products such as gums, barks and fibres. With nearly 50% of land covered in forest and 60% of harvested wood processed in Europe, this is therefore a significant industry for the region.

The forest products industry - consisting of industrial roundwood, sawnwood, wood panels, sheets and wood fuels - was estimated to be worth 105bn€ in 2019.4 Of which (and the focus for this PLI report) 76bn€ was generated by the sawmill industry - the extraction of timber and processing it into planks.5

Definition, segments within the industry and market share

Fine and coarse wood, sawdust and bark produced during wood processing at sawmills, veneer mills and furniture manufacturers.

Whole trees from forests, plantations, orchards etc. include those harvested specifically for energy, those removed as part of commercial thinning operations, disease or death, and those removed to reduce forest fire potential.

Materials resulting from tree collection/harvesting operations and include treetops, twigs, and branches.

4

Whole trees

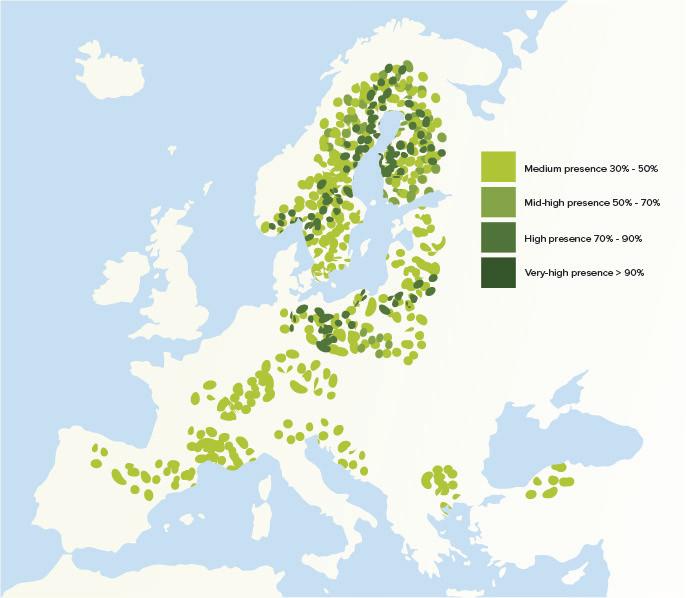

Land area covered by forests in Europe in 201912 Sawmills operating in Europe13 Country/region % Country/region % Country/region % Country/region %

for approximately 5% of the world's forests and, contrary to what is happening in many other parts of the world, the forested area of Europe is slowly increasing.7 As of 2020, 23.6% of Europe’s forests were in protected areas with most European forests having designated management plans in operation, and the highest percentage globally of forestry management plans.8

66 Spain 37 Germany 32 Denmark 15 Sweden 64 Portugal 36 Italy 32 United Kingdom 13 Slovenia 58 Bulgaria 35 Poland 30 Ireland 11 Estonia 54 Luxembourg 34 Greece 30 Netherlands 8.9 Latvia 53 Croatia 34 Romania 29 Malta 1.5 Austria 46 Czechia 34 France 27 Slovakia 39 Lithuania 34 Belgium 22 EU overall 38 % Country/region No. Country/region No. Country/region No. Country/region No. Sweden 184 United Kingdom 19 Czechia 7 Ukraine 3 Finland 92 Denmark 18 Romania 7 Slovenia 2 Germany 82 Switzerland 18 Italy 6 Bulgaria 1 Austria 46 Estonia 16 Slovakia 6 Hungary 1 Russia 38 Latvia 15 Spain 6 Netherlands 1 France 33 Poland 13 Belgium 3 Norway 25 Lithuania 11 Ireland 3

Alongside a high proportion of forest coverage, there are over 650 sawmills operating in the EU.11 Whilst 25% are based in Sweden alone, across the remaining EU-member states, there are on average nearly 20 sawmills. These sawmills, in turn, are heavily relied upon by forest-based industries, including woodworking; pulp, paper and paper products; printing; construction; furniture products; and wood bioenergy (often interlinked with other industries).

Approximately 1.1m 3 of wood is consumed per capita in Europe. 10 Much of this demand is from the construction sector, however this slowed down during the COVID-19 pandemic when many construction activities were forced to halt work. During this time, there was instead a surge in demand for paper, paper products and packaging, as online shopping and deliveries increased significantly.

Forests cover a total of 31% of the globe, a percentage which is decreasing. It is estimated that over the past decade, 4.7 million hectares (0.1%) of forests have been lost worldwide. In contrast, Europe has a higher coverage of forestry (46%), and specifically in Finland, Sweden, Slovenia, Estonia and Latvia, over 50% of land is Europecovered.6accounts

Finland

5

Globally, approximately 30% of forests are used primarily for production, with Sweden being the largest forestry product producing country in the world, tied with Canada.9

Market size and coverage

Growing stock in Europe by main species18 OtherFirBirchOakBeechSprucePineSprucePine30%23%Beech12% BirchOak10%7%Fir3% Other15%

In 2018, over 500,000 employees worked in the forestry and labour sector, a 2% decrease since 2000. Poland employs the largest workforce, followed by Romania, Sweden, and Germany respectively. However, productivity of labour is heavily influenced by the size and locations of the forests, as well as the labour intensity of the sector.15

Gross value added to EU economy by country in 2018 (million Euro)14 200010005000150025003000350040004500

Finland France Germany Sweden Italy Romania Poland Czechia Austria Spain

Employment in forestry and forest-based industries is of significant importance to rural areas where most forests are located.17 Regional differences such as this are highlighted by labour per hectare of forest where in Norway and Sweden there is one person per 1,000ha compared to in Hungary, Slovakia and Republic of Moldova with over 10 persons per 1,000ha of forest.

This is a result of the increased automation and mechanisation utilised in Northern Europe, as well as the physical makeup of forests and their accessibility. This is again reflected in the Gross Value Added per employee which is significantly higher in Northern and Central-West Europe where there is increased mechanisation.

6

Of those working in forestry and forest-based industries, 36% are employed in the primary forestry sector, 40% work in wood manufacturing, and approximately 25% in paper. However, this varies according to region. For example, in many South-Eastern countries in Europe employment is greater in the primary forestry sectors compared to Central Europe where there is greater employment in wood working and paper-based industries.16

Current uses

Wood

Characteristics

Lifespan 200-300 years

Type Deciduous

Wood

Orange bark on upper stem, blue/grey-green needles 5-7cm long in pairs, can tolerate cold, drought and poor soils, cones carrying seeds are green and ripen to brown after two years.

Current uses

Scots Pine19 | Pinus Sylvestrus

Type Coniferous

Lifespan 150-300 years

Single-stemmed, silver-grey barked trunk; high growth rate until mature age; leaves are elliptic, dark green and shiny.

Softwood – one of the strongest, with a good strength to weight ratio. Easily workable. Lasts well in wet conditions. Commercially and economically important, particularly to Nordic regions.

Current uses

Having approximately 250 known usages, its diversity makes it one of the most important species in Europe. It is ideal for boatbuilding, flooring, stairs, furniture, musical instruments (piano pinblocks), plywood, panels, veneering and cooking utensils such as bowls, platters and wooden spoons. It is also used for pulp and can be coppiced for firewood and charcoal due to its high energetic potential.

Sawn timber for building, construction, furniture, pulp and paper. Due to its plant hardiness in poor soils it is also planted for land reclamation, anti-erosion and windbreaking.

Norway Spruce20 | Picea abies

Size 30-40m average, 50m maximum

Size 23-27m average height

Lifespan Up to and over 400 years

Wood

Characteristics

European Beech21 | Fagus Sylvatica

Hardwood – strong, fine-grained, knot-free, pale cream colour, bendable and easy to work, wear-resistant.

Orange-brown bark, creamy white wood, cylindrical 12-15cm long cones are green then turn brown in autumn.

Softwood – easy to work if no knots are present. Not particularly durable, decay-resistant or tough.

7

Characteristics

Profiles of the top three species of trees

Type Coniferous

Solid wood for timber construction; pulpwood for paper; joinery timber; furniture; veneer; tone-wood (sound boards of pianos and the bodies of guitars and violins); most common Christmas tree.

Size Up to 50-60m height, up to 150cm diameter trunk

Additional biomass for energy may be derived from harvest slash (e.g., branches, tops, stumps) that would otherwise have decayed in the forest. This tends to be a low-value product compared with other forest products, and thus not traditionally a primary driver in determining forest management and harvest scheduling.

In 2017, of 31 countries in a study, wood energy accounted for 3.8% of total primary energy supply and 35.4% of renewable energy supply – the highest source of renewable energy. Woody biomass meets 26.2% of primary energy demands in Finland, 19.6% in Estonia, 19.3% in Sweden, and 17.3% in Lithuania.

Forestry-based biorefineries are spread somewhat evenly across Europe, though there are a considerable number in both Finland and Sweden. Finland and Sweden, as well as Portugal, appear to also have more extensive biorefineries and biorefinery methods.

European sales data and evolution

8

liquor produced during the kraft pulping process is used by the forest industry in wood processing.

In terms of renewable energy supply, woody biomass accounts for over half the supply in Austria, Belarus, Czechia, Estonia, Finland, Lithuania, Serbia, Slovak Republic, Slovenia, and Ukraine. Nearly 43 of total mobilised woody biomass is used for energy purposes.25

Presently, the building industry produces 25% of global greenhouse gas emissions and therefore the concept of green building construction has evolved, expected to reduce CO2 emissions and store carbon. Wood-constructed buildings also produce less waste and can be constructed more quickly than concrete producedbuildings.23e.g.,black

Of forestry-based biorefineries in EU member states, 57.1% use primary biomass (materials specifically for creating bioenergy) and 42.9% use secondary biomass (converted or decomposed forest materials).24

Forest-based bioenergy is a common coproduct of the forestry industry and is the second most important biorefinery method in Europe after agricultural feedstock. It can be done using either primary forest materials (collected with the specific intent to use as bioenergy) or secondary forest materials (collected as a byproduct of other forestry activities).

Wood used as a building material is increasing due to numerous advantages of wood buildings over concrete buildings, and promotion by governments and the industry itself, thus driving the market for forestry and logging producers.

ForestConstructionbioenergy

Accounting for over 43% of the global forestry and logging market in 2020, the construction segment is the largest segment by end-use application. It is also expected that this segment will be the fastest growing segment in the coming years, at a CAGR of 10.3%.22

As of 2017, nearly 80% of wood energy is consumed almost equally by industry (39.3%) and end consumers (40.3%). The power and heat sector account for a large share of the energy

Sawnwood production and consumption in Europe (million m3)26 Roundwood production in Europe (thousands)27 6005002001000300400 Europe Produced Consumed Worldwide 80868482787674727068 Removals Consumed 2015 2016 2017 2018 2019

Current and future market trends

The coronavirus outbreak hit Europe very unevenly. In countries where the economy was more resilient – such as Scandinavia and Germany – and where the construction market held up better than expected, the sawmill industry has been navigating the crisis quite well. Some segments, such as the DIY sector and home improvement did very well as people spent more time at home and on home improvements. Other countries, such as the UK and those in Southern Europe had a much harder time with construction markets being more severely impacted and sawmills in some cases forced to suspend operations.29

Effect of COP26 on consumer behaviour

There is heavy pressure from both consumers and governments on corporations to put greater focus on the environmental impact of their activities; the EU’s aim for carbon neutrality by 205030 possibly having the largest effect as it regulates many aspects of the forestry industry. As a result, many organisations in forestry and its related industries are committing to sustainable forestry efforts and tree planting initiatives in order to offset their own environmental impact. For example, the European Organisation of the Sawmill Industry (EOS) includes most EU countries and aims to creates sustainable practice in the sawmill industry. Even tech giant Apple invested $200 million into forest restoration and planting initiatives as part of their goal to reach carbon neutrality by 2030; and UK-based global brewery Brew Dog achieved carbon negative status in 2020 through its partnership with Eden Reforestation Projects.

Although wood and wood-based products are used every day as paper, furniture, in construction, for packaging, and in many other areas, including renewable energy; today we are using much less wood compared to the growth of the forest. EU forests have been a continuously growing natural resource in the past 75 years. However, there are doubts as to the longterm benefits of this, as much of this growth has occurred in warmer, drought-prone regions of Europe. As a result, the expanding forests’ productivity and quality plateaus where there are insufficient water levels to accommodate them. This has been the case in the US where farmers have begun cutting down neighbouring trees as they are depleting the water in the region’s soil.31

Effect of COVID-19 on consumer behaviour

The world’s largest e-retailer, Amazon, which accounts for more than a quarter of all e-commerce sales in Germany, reported an increase in sales of almost 26% in the first quarter of 2020 compared to the same period in 2019.

Wood-working production by sector, 201828Woodand wood products Pulp, paper and paperboard Printed FurnitureBioenergyproductsproducts23%29%18%23% 7%

The global pandemic has resulted in a significant increase in consumers’ online shopping and delivery orders during government-imposed lockdowns that required them to stay at home. This has resulted in a surge in demand for paper packaging used for both online orders and food deliveries. For example, over 2014-2019, e-commerce revenues in Germany grew by 63%, and the COVID-19 pandemic created more incentives for businesses in Europe’s biggest economy to adopt e-commerce and increase their presence online, as most retail outlets shut their doors in spring 2020.

The average harvesting rate of the Net Annual Increment (NAI) of forests available for wood supply is officially estimated to be at 63%, with differences among countries. This means wood industries can grow whilst maintaining, or increasing European forest resources. The sustainability of the NAI in Europe can be greatly seen by the European figure of import reliance for industrial roundwood, which has stayed below 10% in the last 15 years.32

Of 20 regions surveyed around the world, the EU was the largest producer of roundwood (sometimes referred to as removals, which consists of all wood removed from forests, other wooded land, and other tree felling sites) and sawnwood. In 2018, roundwood production in Europe was at 650 million m3, making up 32% of global production. This was followed by the Northern America (USA + Canada) and Asia-Pacific regions, who both produced 519 million m

10

Workforce knowledge and experience

Challenges industry, and the production line / processing, is not as extensive as seen in the older workforce, especially as the reliance on advanced technologies increases. For example, knowledge of the specification and requirements of specialist attachments in chain is heavily required in the processing of timber.

Root rot is another common issue affecting the health of forests and their ability to produce healthy, usable wood materials. The challenge faced is how easily the rot spreads via root-toroot contact, affecting neighbouring and next generation trees. Methods to combat this threat include maintaining the condition of tree bark and cutting during winter months when the fungus is less active. In Sweden, 15% of Norway spruce (the most common native species and most susceptible to root rot) have shown decay resulting from the fungus. The estimated cost of root rot to Swedish forestry is 1 billion Swedish Krona – nearly 100 million€.38 Poor quality wood results in lower value, and often logs are even unusable as timber etc. Given that these trees may have been growing for decades or even centuries, this is also a huge loss in terms of time and land use.

Forestry is currently suffering from an aging crisis where a large percentage of its workforce is reaching retirement age and the industry is struggling to attract enough young workers to replace them. This has been further compounded by the global Precision Forestry industry - using tools and technology for site-specific management - which has seen considerable growth as the forestry industry strives for technological advancement that will improve efficiency and lesson the need for larger workforces in forestry. The global precision industry is estimated to be worth 7.2 billion€ by 2024.36

As a large proportion of the workforce reaches retirement age, the depth and range of knowledge of the specialist areas in the

The European forests, particularly in Central Europe, have been affected by a bark beetle proliferation caused by several factors including climate change. According to recent studies, damaged wood due to bark beetle may reach in total 750 million m3 between 2017 and 2026. The European Sawmill Industry has voiced the importance of providing real-time, comparative, science-based and balanced information on European forest resources aiming at forecasting changes and their consequences on forest’s health and raw material supply.37

Forest health and raw material supply

Did you know? It is possible in a single sawmill to find 20km of one type of chain with assorted fittings. Sawnwood production in 201834 22%EU China18% ofRestworld43% 17%US

Although they are continuing to grow, there are significant threats to European forests. The main challenges being faced are environmental issues regarding forest health and other related economic factors. There are also challenges which pertain to the EU forest strategy for 2030 – a key initiative of the European Green Deal which aims to reach carbon neutrality by 2050. The strategy will contribute to achieving the EU’s biodiversity objectives as well as a greenhouse gas emission reduction target of at least 55% by 2030 and climate neutrality by 2050. It recognises the central and multifunctional role of forests, and the contribution of foresters and the entire forestbased value chain for achieving a sustainable and climate neutral economy by 2050 and preserving lively and prosperous rural areas.35

Innovation

Forest modelling and forest visualisation is carried out to survey land and existing forests in order to practice better management of forests and their ecosystems. Doing so enables forests to be planned, mapped and constructed according to appropriate soils, natural environments, climate, and the needs of the forestry industry. To implement forest modelling and visualisation, a variety of technology and tools are necessary, many of which are often in short supply or need further development.

Site management and working environment

Mixed species forests, or simply mixed forests, have proven to result in more productive and fast-growing forests because of their resilience to changeable climate conditions. However, it has also shown to affect the quality of wood and logs produced, particularly in the quality of knotted wood surfaces.

The sustained yield concept aims to consistently produce more than the loss from disruptive means such as fires, insects, disease, etc. This is often done through replanting of seeds, seedlings, and cuts, in accordance with a calculated rotation period. Rotation periods for pulpwood for example, may be estimated at approximately 50 years, whereas softwood sawlogs typically require 100 years, and broad-leaved trees (like central Europe’s beech and oak) may require as many as 200 years to mature, making the sustained yield practices integral to ensuring supply.39

For example, Metsä Fibre - a producer of pulp, sawn timber, and bioproducts - is building a new sawmill in Rauma, Finland. Metsä Fibre hopes that this new sawmill will produce around 750,000 cubic metres of pine sawn timber each year, thanks to machine vision and artificial intelligence. It will also enable the 100 direct employees at the site to move from workstations around the production line to control room monitoring.40

Another significant challenge for sawmills to consider is the working environment and ability to process the natural resources that may have imperfections or impurities that can affect machine operations and required maintenance, such as strong bark or excess branches. As a harsh environment, all equipment and components must be able to address these challenges.

Key producers* in the forestry industry41

Given that approximately 12.5% of delay time in most sawmills can be attributed to the running out of logs, efficient handling of raw materials in the receiving yard and proper routing of finished products is vital for forest-based industries. Wood-yards must be designed to facilitate rapid separation of species and wood type to aid uniformity of the final products and improve energy consumption during handling and processing.

*Producers included in this list may also operate in other related industries such as paper or packaging, as well as in the processing of timber.

(asRankof 2020) Company Headquarters No. of sawmills Production in 2020 (1,000 m3) 1 Stora Enso Finland 18 4,690 2 Binderholz Austria 8 3,180 3 Vida Wood Sweden 12 2,350 4 Pfeifer Holz Austria 5 2,080 5 Moelven Group Norway 15 2,060 6 SCA Timber AB Sweden 5 2,000 7 HS Timber Group Austria 4 1,980 8 Mayr-Melnholf Holz Holding AG Austria 3 1,950 9 Rottenmeier Holding AG Germany 5 1,900 10 Södra Timber Sweden 7 1,900

Docma S.r.l | www.docma.it | Verona, Italy45

C. Gunnarssons Verkstads (CGV) AB | www.cgv.se | Vislanda, Sweden44

Dragon Machinery | www.dragon-machinery.co.uk | Oswestry, United Kingdom46

It is worth noting that across Europe the spread of machine equipment manufacturers and builders can be quite varied. For example in Austria and South Germany there are a higher number of smaller manufacturers, whilst other regions in Europe may be more heavily saturated with larger organisations.

Whilst predominantly providing shredding, shaving, and recycling services, Dragon Machinery manufacture and design a range of sawmilling and specialised timber processing machinery for waste wood to be shredded according to input size, type, volume and output size required. Dragon Machinery also offers a bespoke design service for other sawmilling applications, such as log decks, step feeders and log hauls.

AS Hekotek | www.hekotek.ee | Harju Maakond, Estonia48

Henkon Forestry B.V. | www.henconforestry.nl | Ullft, Netherlands49

There are over 7,200 manufacturers of machinery used for forestry and agriculture in Europe, with a 30% market share, equating to 2.4 billion€. Global demand for forestry equipment is rising, with a projection of exceeding 11.5 billion€ by 2027.42 The forestry equipment market is usually segmented by product type – felling, extracting, onsite processing, and other forestry equipment. Chainsaws, harvesters, and feller bunchers are all part of felling equipment.43

Part of the Lifco AB Group, Heinola Sawmill Solutions manufacture bespoke drying kiln solutions, as well as chippers for sawmills to create high quality fuel chips, and large drum chippers for the pulp and paper industry.

Providing machines and equipment to the sawmill industry for over 60 years, CGV primarily operate in the European market. Machine and equipment include dry sorting and high-speed planer mills. With expertise in sorting, they also work with customers to develop automation systems to improve controlling sorting facilities for increased capacity and greater efficiency.

Heinola Sawmill Solutions | www.heinolasm.fi | Heinola, Finland47

Built in the Netherlands and Italy, Hencon Forestry manufacture forestry tillers and rotavators, wood clamps, tree shears and chain saw systems for the collection of wood in less accessible areas. In addition, their range extends to the biomass industry for the collecting, chipping and grinding of trees and forest residue.

Also part of the Lifco AB Group, Hekotek are one of the leading manufacturers of machinery used in sawmills, offering a complete turnkey solution, such as log sorting lines, conveyor systems, board handling lines and log infeed lines. Based in the Baltic states, Hekotek supplies sawmill equipment across Europe. In 2020, they reported sales of c. 2,500 million SEK.

Major machine & system builders

Operating across the agriculture, forestry, construction, and mining industries, Docma specialises in the manufacture of winches, log-splitters and saw benches. Located in Verona, Italy and with over 20 years of experience, they provide portable machinery for the early stages in the production of timber, where logs are felled and collected for taking to the sawmill.

Prior to being acquired by USNR, Söderhamn Eriksson specialised in log lines and edger systems. Now as part of USNR, the range extends to complete end-to-end solutions for sawmills and planer mills. USNR also produce equipment for the manufacture of plywood and other panel products, and products to scan, grade and handle veneer and panel products.

SERRA | www.serra-sawmills.com | Rimsting, Germany54

Primultini s.r.l. | www.primultini.com | Vicenza, Italy52

USNR | www.usnr.com | Söderhamn, Sweden56

Wood-Mizer Industries | www.woodmizer-europe.com | Koło, Poland58

A global market leader in technologies for plywood and laminated veneer lumber, Raute manufacture equipment for the processing of timber into engineered wood products. From their European offices in Finland, they offer complete turnkey solutions, as well as individual components and automation technology such as machine vision and analysis. In 2020, Raute reported sales of 115 million€.

TKM GmbH | www.tkmgroup.com | Remscheid, Germany55

A world-leader in portable and stationary narrow band sawmill and bandsaw blades, Wood-Mizer is well-known across the forestry and sawmill industries. From forest to sawmill, WoodMizer produce machines used throughout the production process, including vertical saws, resaws, edgers, planers, slab flatteners, blades, and maintenance. They also can design smart-log processing lines, identifying opportunities to automate elements of the production line.

Kallion Konepaya Oy | www.kara.fi | Laitila, Finland50

As well as forestry machinery and equipment for the gathering of timber, SERRA manufactures sawmills with computer-assisted 3D programs for a bespoke solution. In addition, they offer edgers and resaws to process sideboard and main boards across slats, beams and boards, depending on the need, and to help relieve the reliance on the main saw alone.

Raute | www.raute.com | Nastola, Finland53

Providing a complete solution for sawmills, from timber handling and conveying to debarking, measurement and sorting, the Primultini Group also specialise in band saw blades through their brand Mec-Legno and automation services with the brand PriBo.

Uniforest | www.uniforest.com | Prebold, Slovenia57

As a group of four companies, Ledinek position themselves as experts in the complex processing of large wood, planing and profiling, finger jointing and design, delivery and installation of cross laminated timber panel production lines. They also provide specialised solutions for the automation of destacking, quality grading and marking and conveying systems.

More than just “knife manufacturers”, TKM operate across a variety of industries including paper, print and packaging, metal, plastics, food and the wood industry. TKM manufactures saws and industrial knives such as circular saw blades for precutting, profiling, edgers, chipper canters, and accessories. Their extensive knowledge of knives is paramount for identifying the right knives and accessories to use for the intended material and to reduce the risk of tarnishing and stains on the finished product.

Manufacturing forestry machines such as winches, log splitters, crane grabs, and circular saws, Uniforest is a leading manufacturer in the forestry industry. Their products are primarily used in the collection and initial preparation of timber before it is transported to the sawmill for processing and finishing.

Ledinek | www.ledinek.com | Hoče, Slovenia51

A leading manufacturer of one-blade circular sawmills, Kallion Konepaja Oy’s brand– KARA – has a selection of cross-cut saws for trimming, crosscutting and component cutting of timber, as well as processing waste wood and slabs for firewood. The brand has over 100 years of expertise in saw technology and has expanded from saw blades to designing and developing complete sawmill lines and solutions.

Any logs with remaining metal are sent back for a secondary examination. If the metal can be removed the whole log continues down the production line. If not, the log is salvaged in small sections.

Process Debarking

6. Waste

5.

Introduction

Logs are debarked using mechanical ring cutters, cambio drums or waterjet blasters. This safeguards saws and other equipment from undue wear and damage that would otherwise result from stones, metal and other contaminants embedded in the bark.

Production of timber logs conveyor Breaking down

debarker edger scanner 7.

Infeed, and sorting

Logs are scanned, measured and graded, and sorted according to species, diameter, length and end-use.

Unused bark from the debarking process is stored and burned for heat energy used in the drying process. This typically accounts for 70-90% of total energy consumed in the sawmilling process.

Waste sections, or slabs, are recycled into chips, pellets, or mulch.

4. Sizing and sorting Debarking conveyor

4 5 6 7 log decksorted

An initial saw sees the log broken down into slabs, flitches and cants. This sets a flat surface to square the work for secondary cants that turn into rough sizes for finished lumber products.

This schematic describes the typical process used for the processing of timber from extraction to the sawmill.

This process, whilst being typical, does not represent all processing and extraction of forestry. This is because actual plant processes may vary according to the desired end product - for example construction, paper and furniture.

14

scanning

PART TWO productionSawmill line intelligencemarket

waste

Multiple blades reduce the large-cut cants to smaller sizes according to the required use.

Log ladder and

2. Transportation

1. Felling

9. Resawing

3. Infeed

A log ladder/carriage conveys the log through the headsaw (head rig) on which the log may be clamped to a conveyor and turned. Depending on the sawmill, the conveyor may be a stationary carriage whilst the head rig moves through the log; or the head rig may be fixed whilst the log moves on a mobile conveyor.

15 Collection of raw material

Process

The felled logs are received by the sawmill and transferred onto the log deck by heavy lift trucks, derricks or cranes depending on the logs' dimensions and weight.

Vehicles equipped with lifting gear and grabbers transport felled logs to the sawmill. Alternatively, if available, logs are sometimes transported downstream, by river.

123 8 9

sawing

Loggers cut or fell standing trees, before being loaded for transport to the sawmill site. Winches and saws are occasionally used on site when in tight-closed spaces.

fixed saw headsaw log ladder / carriage

8. Headrig / primary breaking down

10 11 12 17

Production of timber vertical sorter horizontal

Final preparation

17. Packing, storage and transportation

Rough round edges are removed either by a circular saw or a chipper edger. This is to produce standardised widths and lengths, with edges squared and defects removed. This can be by one or more trimming saws.

The dried timber is sorted for final inspection of any defects that may have occurred during the drying process. These can be removed with trimming, before being packed and stored in warehousing, to then be transported for further processing of woodbased products.

sorterplaner

Process

16 Log ladder and sawing

packaging & storage transportation

10. Edging and trimming

11. Sorting

The cut lumber is then sorted by lengths, species and dimensions into bins to then be placed onto palettes for easy transportation and storage.

17 sawing Seasoning

13. Sealing timber

14. Air drying

15. Kiln drying

16. Planing

To protect the sawn timber against fungi and insects, and to inhibit the tendency of airdried lumber to check and split, the ends may be brushed, dipped or sprayed in a suitably prepared chemical solution. This acts as a sealant in order to bring about a slower and more uniform drying process.

The sawn timber is stacked into piles out in the open or under sheds where they are exposed to good air flow.

12. Stacking

Once the lumber has dried, it is taken to the planer infeed. This is where the timber is given final shaping and its smooth finish and appearance.

13 14 1516

The sawn and trimmed timber is sorted according to thickness, width, length, quality, grade and species, depending on market requirements. This can be done manually or by mechanised sorters.

Alternatively, the sawn timber is stacked in a closed and controlled environment where temperature, air circulation and humidity is regulated so to achieve the most economical drying conditions without affecting the timber. Batch kilns dry the timber in chambers as a batch charge, whilst progressive kilns dry the timber as it passes through the kiln on trucks.

Process air drying shed

kiln drying shedplaner infeed

• Belts - synchronous belts, timing belts, v-belts, and belt drives and pulleys

• Chain - conveyor chain, roller chain, supporting profile, and chain oil

• Flexible claw

• Grease

• Grease

• Pumps

• Chain - conveyor chain, roller chain, chain sprockets, chain tensioners, and chain oil

4 log

• Slewing rings

• Chain sprockets

Critical projects and opportunities

• Bellows

Infeed, scanning and sorting

Critical projects and opportunities

Production of timber

• Adapter sleeves

• Swing drive

• Fans

• Flexible couplings

• Hydraulics - silent blocks

• Plain bushings

• Plastic wrap

18 Process

4. Sizing and sorting decklogs

• Shaft-locking devices

• Gear drives

• Synchronous belts

• This part of the process in the sawmill is often over-loaded with high impact and vibration. Overhung loading can affect the gear drives, chain and bearings.

• Plummer block housings with reinforced designs are often used.

• Blowers

• Rod ends

• High durability is critical to handle shock and perform under load.

3. Infeed

Debarking

Explaining the opportunities and projects

Key critical projects within the sawmill have been highlighted along the schematic to make it easy to identify which areas of the process have most opportunity.

• Chains run dry, without lubrication, due to the amount of sawdust in the environment. Annual replacement of chain. SOV: 50 - 100k €.

• Bearings - filament bearings, housed bearings, plummer block bearings, and spherical roller bearings

sorted

• Sold steel units

scanner

Key product groups

• Replacement of rubber conveyor belt used in scanners. SOV: 10 - 15k €.

• Adapter sleeves

• Bearings - flange bearings, housed bearings, spherical roller bearings, and split bearings

• Couplings

Key product groups

• Individual cost per slewing ring. SOV: 15 - 20k €.

• Plain bushings

Critical projects and opportunities

• Sprockets

• Bearings - spherical roller bearings, and tapered roller bearings

• Plastic wrap

• Winches are sometimes used with chain and conveyor inside.

Log ladder and sawing

• Belt drives

1. Felling

• Couplings

• Chain is used to pull on the tree with a special "U" attachment to get grip onto the tree and pull it through the knives for the cutting mechanism.

• Grease

• Saws

• Plastic wrap

• Chain

Collection of raw material

1

Process

• Hose, hose assemblies and adapters

• Turntables

• High-wear environment, where chain needs to be replaced frequently.

Critical projects and opportunities

• Harvester head supports the tree and de-limbs it. The tree is then cut to length.

Key product groups

• Truck-mounted crane

• O-rings

• Belts - synchronous belts, timing belts, and v-belts

Key product groups

• Slewing rings

• Hose, hose assemblies and adapters

2. Transportation 23

• Hydraulics

19

• Seals

• Gear motor

• Grease

Key critical projects within the sawmill have been highlighted along the schematic to make it easy to identify which areas of the process have most opportunity.

• Shaft-locking devices

• Some smaller debarkers use drive belts - in a very harsh environment where wood and bark pieces fly around, belts can be cut regularly with open drives.

• Link belting is sometimes used as an alternative as it is made from durable material that can withstand cuts from wood chips due to being pre-tensioned and the ability to replace individual links rather than the entire belt. Swap from drive belts to link belting - SOV: 1k € cost-saving.

• Alternatively, rubber conveyor belts can be used in waste conveyors. SOV: 5k €.

Critical projects and opportunities

5. Debarking 6. Waste conveyor 5 6 7 debarker edger waste conveyor

Production of timber

Key product groups

• Couplings

• Gear drives

• Hydraulics

Explaining the opportunities and projects

• Solid steel units

• Bearings - housed bearings, spherical roller bearings, and split bearings

• Grease

• Belts with metal rivets can be used by metal detectors to scan for debris.

• Without proper maintenance, bearings in pelletizers can require replacement every 500 hours. Installing high-performance spherical roller bearings can increase bearing life by five times, operate in cooler temperatures, and require less maintenance.

• Belts - synchronous belts, rubber conveyor belts, v-belts and belt drives

• Annual instalment of pan grinder rollers adjusted for taper roller bearings to improve service life by 3 times. SOV: 4k € for two presses.

Process Debarking

Infeed, scanning and sorting

• Hose assemblies

20

• Conveyor chain

Critical projects and opportunities

• Hydraulic drives

• Belts - synchronous belts, and v-belts

• Pumps

• Solid steel units

• Power packs

• Fans

• Saws

• Waste can be transported for use elsewhere e.g., bioenergy, pulp, or can be even used in ovens to generate heat for dry installations.

• Power packs

• Bearings - cylindrical roller bearings, filament bearings, spherical roller bearings, split bearings, and housing units

Key product groups

• Chain - conveyor chain, leaf chain, roller chain, and chain oil

Critical projects and opportunities

• Chain - conveyor chain and chain oil

• There is a lot of dust in this part of the process, with heavy loads on all components.

• Several options for headrig and primary breaking down: headrig, center line, band mill and vertical or horizontal gang edgers

9.

8 9

Critical projects and opportunities

Process

Key product groups

• Grease

• Bearings - housed bearings and spherical roller bearings

• Conveyor chain and technology

7.

• Extended length belts (up to 20m long) are ideal for these types of environments, compared to the equivalent chain. Extended length belts are much lighter and energy-saving. & 8. Headrig + breaking down Resawing

fixed saw headsaw log ladder / carriage

• Belts - synchronous belts and v-belts

21 Collection of raw material

Log ladder and sawing

Key product groups

• Belts - synchronous belts and v-belts

• Hydraulics

• Bearings - housed bearings and spherical roller bearings

• Gear motor

• Grease

• Adapter sleeves

• Grease

• Pneumatics

Production of timber

• Stacking systems also use rollers similar to those in the sorting process. These can be hard to replace due to the need to lift the rollers to re-install the belts.

horizontal sorter

Explaining the opportunities and projects

• Ball bearings

Key product groups

Log ladder and sawing Process

• Some trimmers are connected via tubes, and take the sawdust to a container to go to paper plants. The sawdust must be clean, but sometimes rubber belts can elongate and break, causing pieces of rubber to mix with the sawdust.

10. Edging and trimming

10 11 12

11. Sorting

Final preparation

• Gear motor

Critical projects and opportunities

• Helical gearboxes

Critical projects and opportunities

• Chain - conveyor chain, roller chain, and chain tensioners

• Shaft-locking devices

• Bearings - ACIS proof bearings, spherical roller bearings, split bearings, and housing units

• Welded steel chain

• Bellows

• Belt - conveyor belts, synchronous belts, timing belts and pulleys, and v-belts

• Belts - synchronous belts and v-belts

• Bearings - ball bearings and flange bearings

• Slewing rings

• Grease

• V-belts on trimmers can wear very quickly due to significant dust and movement of blades.

• Replacement of rubber conveyor belt. SOV: 5k €.

• V-belts

• Solid steel units

• Shaft-locking devices

• Depending on the length of the line, swapping to link belting can save between 5 - 15k € annually.

• Roller chain

Key critical projects within the sawmill have been highlighted along the schematic to make it easy to identify which areas of the process have most opportunity.

• Locking elements

12. Stacking

vertical sorter

• Hydraulic drives

Critical projects and opportunities

22

• Big rollers are hung up mid-air and driven by rubber v-belts (4 - 6 belts per roller). Each roller can weigh up to 60kg.

• Classic v-belts can be hard to replace in this remote area of the production line, with severe health & safety risks due to the wetness and dust in the environment.

• Replacing banded belts with link belt. SOV: 25k € cost saving.

• Split clutches

Key product groups

Key product groups

• Bearings - ball bearings and split bearings

kiln drying shed

Process air drying shed

14. & 15. Air + kiln drying

Seasoning

• Shaft-locking devices

Key product groups

• Couplings

Critical projects and opportunities

• Pneumatics

• Link-belting is resistant to chemical and high heat exposure, meaning the belts can last for over 15 months without needing frequent service.

• Belts - synchronous belts and v-belts

• Many sawmills make their own customised kiln designs.

Key product groups

13 1415

• Bearings - ball bearings and filament bearings

13. Sealing timber

• Gear motor

23

• Blowers

• Chain - leaf chain and roller chain

• Heaters

• Pillow blocks

Production of timber

• Grease

• Using split couplings to reduce time invested, cost and production downtime. SOV: 10k €

Process

• Seals

• O-rings

Explaining the opportunities and projects

17

• Belts with 14mm pitch have high strength, good environmental resistance and require minimal maintenance and lubrication.

• Replacement of all housed units to solid block housed units with seal encapsulation. This can extend the lifetime of the application by 20+ times, where previously the bearings would need to be replaced often due to the high wear in extreme conditions. SOV: 10k €

• Pneumatics

Critical projects and opportunities

transportation

• Plain bushings

Log ladder and sawing & storage

• Linear guidelines

Key product groups

• Bearings - ball bearings, flange bearings, spherical roller bearings, and tapered roller bearings

• Belts - synchronous belts and v-belts

• Slewing rings

planer packaging

Key critical projects within the sawmill have been highlighted along the schematic to make it easy to identify which areas of the process have most opportunity.

17. Packing, storage and transportation

17. Packing, storage and transportation

• Chain - flyer chain, leaf chain, roller chain, and chain tensioners

24

• Shaft-locking devices

• Conveyor technology

Final preparation

• CAM followers

16

• Flexible claw

16. Planing

25

Key product groups

• Belts - synchronous belts and v-belts

• Bellows

• Bearings - ball bearings, spherical roller bearings, split bearings, and housing units

• Couplings - disc couplings and flexible couplings

Process

planer infeed

• Linear guidelines

Production and processing of timber – ‘Putting it all together’ Proportion of replacement products in the sawmill Bearings Chain Hydraulics and fluidLpowerubricationLinear guide Belts Couplings Otherseals,includinggears,andmotors 30% 25% 14% 9% 9% 6% 4% 3% 1234 5 6 7 8 9 Collection of raw material Debarking Log ladder and sawing Infeed, scanning and sorting

Production of timber

26

27 The approximate value of PT aftermarket sales in the European sawmill 300mindustryeuros 10 11 12 13 14 151617 Log ladder and sawing Final preparation Seasoning

An extraction site of raw materials with winching and sawing capabilities?

The size and throughput?

a. Detail of the company itself

• What kind of questions will you ask (in relation specifically to who will be seen)?

• Who decides on purchasing?

3. The follow up – questions to ask or to reflect on, at the end of the meeting or afterwards

• What are you visiting?

Its scale in terms of capacity, output etc?

What type of tree do they typically have access to in the region and/or process e.g., pine, spruce or beech etc.

of these questions you may already know the answers. Others might be used on a regular basis when you visit customers and prospects in other industry sectors. It is meant as a resource to act as a prompt and reminder allowing your business to fully capitalise on this market intelligence and production information.

• What is your initial summary as to the main challenges they face in relation to purchasing the types of products you can supply?

A sawmill - from sorting, screening, debarking, planing and distribution?

• How old is the facility?

BreadthPresentationExploratoryofservice

• What is your plan for follow ups to this meeting (further meeting/proposal/meeting with other people)?

Using this document to develop business

• Do they have in-house maintenance engineers?

b. The people to be seen and which department

• What are your primary objectives for the meeting –what do you want to achieve?

The 'Extraction Site' or 'Sawmill'

Do the system suppliers provide after market warranty service?

1. Preparing (before any visit takes place) – this provides questions to think about and address before attending the company’s site. This further breaks down into two sections being:

Is this transported by road, rail, or water for processing at the sawmill?

Whether the extraction site or sawmill is specific to a particular end market e.g., construction, furniture, wood-working, or pulp and paper?

The people to meet

2. The meeting – questions to ask during the meeting to understand the needs, requirements, and potential sales opportunities in the prospective customer

There are three parts that deal with:

• What are the fall-back objectives if the primary objectives are unachievable?

• What is their role or speciality (production/maintenance manager/repair/purchasing)?

• Does this company have other facilities in your region/territory?

• What do you know about them already? (hint: search LinkedIn)

• How many people do they employ?

• What kind of support material do you need to take with you?

PART THREE

• What do you already know about:

Forindustry.many

The following provides the reader of this document, either General Management or Sales Team, with some template questions to help generate revenue from this Production Line Intelligence overview and so develop business in the forestry

• Who are you going to see?

General

• What is your proposed agenda?

Preparing – before the visit

28

(If not already known, any of the preparation questions can be asked during the meeting to establish site type, size, capacity, age, as noted).

• What do you value most in relation to a supplier/ distributor like us?

• Do you have existing projects carried out in relation to maintenance or energy management etc?

Are there on-going projects to deal with this?

• What are the next steps you need to take and when?

• What are the next steps? Can we come back with a proposal to help you with some of this?

The follow up

• What sort of regular maintenance does the plant undergo?

• What is the estimated annual spend on maintenance?

Are existing partners – suppliers or distributors – assisting?

• How will you complete these?

• What are the processes used from receipt to dispatch?

LogDebarkingladder and sawing

• How are you going to store this information?

Suppliers

Are you using partners – suppliers or distributors –to assist you in this process?

The facility

FinalSeasoningpreparation - planing, packaging, storage and distribution

29

Regular shut-down periods or other?

• Who in your business do you need to share this information with?

• What kind of support do you look for from your service providers in relation to on-going or emergency maintenance?

• What other types of follow up will you undertake and why? What have been the success stories? How can these be replicated?

Maintenance, planning and issues

• What parts are used most on an annual basis? What are the issues/challenges faced getting those parts?

What are the main issues in relation to maintenance?

• What are the main concerns in relation to type of production parts that are needed to maintain and improve the line e.g., bearings, chain, belts, etc?

• How are you going to use this information?

Internal team, external team, machine builder service engineers?

• What is your biggest current problem with your partsHowsuppliers?doyou like your supplier partners to assist?

The actual meeting 'Extraction Site' or 'Sawmill'

Infeed, scanning and sorting

The most utilised products

• What were the main points you learned from the visit?

• How are the main machines maintained and repaired?

• What are the main issues in relation to maintenance?

• What are the key maintenance/industrial supplies objectives for the facility?

• How will you ensure that these follow ups are completed?

• Where is the process most prone to failure or maintenance problems?

• What sort of plant or facility is this e.g., extraction of timber or processing of raw materials?

• What are the 'bottlenecks' in the process that affect speed or reliability?

What are they caused by?

14.

23. Ibid. 24.

48.

51.

The costed examples contained in this document are illustrations taken from real practice. They are, however, not predictions of future value achievable from various projects that can be undertaken in this sector. The authors, contributors and EPTDA do not accept any liability for any commercial decisions that may be taken as a result of these examples.

9.

53.

50.

41.

13.

2.

57. USNR,

2050:

32. European Panel Federation, ‘EU forest-based industries 2050: A vision of sustainable choices for a climate-friendly future’

8.

Authored by:

25. Ibid. 26.

39.

49.

28.

54.

52.

29.

20.

1. European Commission, ‘Communication from the Commission to the European Parliament, the council, the European Economic and Social Committee and the Committee of the Regions: A new EU forest strategy: for forests and the forest-based sector’ The Business Research Company, ‘Forestry and logging global market report 2021’ European Panel Federation, ‘EU forest-based industries 2050: A vision of sustainable choices for a climate-friendly future’ MarketResearch.com, ‘Forest products in Europe – Market summary, competitive analysis and forecast to 2024’ European Organisation of the Sawmill Industry (EOS), ‘EOS annual report 2019-2020’ Forestry Commission, ‘Forestry statistics 2020 – Chapter 9: International forestry’ Forest Europe, ‘State of Europe’s forests – 2020’ Euroaxess, ‘Labor market briefings series: The agriculture and forestry sector in Europe’ Ibid. Forest Europe, ‘State of Europe’s forests – 2020’ The Sawmill Database, 'Sawmill list by country' Eurostat, ‘Forests, forestry and logging’ The Sawmill Database, 'Sawmill list by country' Forest Europe, ‘State of Europe’s forests – 2020’ European Panel Federation, ‘EU forest-based industries 2050: A vision of sustainable choices for a climate-friendly future’ Food and Agriculture Organization (FAO) of the United Nations, 'Employment trends and prospects in the European forest sector' Eurostat, ‘Forests, forestry and logging’ Forest Europe, ‘State of Europe’s forests – 2020’ Europa, ‘Pinus sylvestris in Europe: distribution, habitat, usage and threats’ Europa, ‘Picea abies in Europe: distribution, habitat, usage and threats’ Europa, ‘Fagus sylvatica in Europe: distribution, habitat, usage and threats’ The Business Research Company, ‘Forestry and Logging Global Market Report 2021’ JRC Publications Repository, ‘Chemical and material driven biorefineries in the EU and beyond’ Forestry Commission, ‘Forestry statistics 2020 – Chapter 9: International Forestry’ EOS, ‘Annual report 2019-2020’ European Panel Federation, ‘Forest-based industries a vision of sustainable choices in a climate-friendly future’ EOS, ‘Annual report 2019-2020’

11.

17.

40.

Acknowledgements and a sincere thank you to the following manufacturer members of EPTDA for the generosity of the technical and commercial information and advice that they have supplied and which has given real authority to the document.

37.

18.

21.

58.

7.

47.

31. BBC News UK, ‘Images show decline of California’s life source’

12.

16.

27.

4.

46.

15.

5.

44.

33. FAOSTAT, 'Global forest products: facts and figures' FAOSTAT, ‘Forestry production and trade’

30Sources:

45.

6.

Disclaimer:

Acknowledgements

Finally to the individual members of the EPTDA Know Your Market Committee and particularly to its Task Group, who have freely given their advice, guidance and inputs throughout the process of producing this document.

36. Markets Insider, ‘Global precision forestry market projected to reach $6.1 Billion by 2024, at a CAGR of 9% during 2019 – 2024’ EOS, ‘Annual report 2019 – 2020’ Forestry.com ‘Root rot – yet another enemy to fight’ The Business Research Company, ‘Forestry and logging market – by type – global forecast to 2030’ Metsä Fibre, 'Rauma sawmill' Timber Online, ‘Europe’s top sawn timber producers’ Global Market Insights, ‘Forestry equipment market size worth over $13bn by 2027’ Fortune Business Insights, ‘Forestry equipment market size, share and industry analysis by equipment type, and regional forecast, 2019 – 2026’ CGV, 'About us' Docma, ‘Company’ Dragon Machinery, ‘About’ Heinola Sawmill Solutions, ‘Company’ Hekotek, ‘About us’ Hencon Forestry, ‘Forestry’ KARA, ‘Company’ Ledinek, ‘Company’ Primultini, ‘Company’ Raute, 'Company' SERRA Sawmills, ‘Company’ TKM Group, ‘The Company’ Uniforest, ‘About us & contact’ 'About us' Wood-Mizer Europe, ‘About’

10.

30. European Panel Federation, ‘EU forest-based industries 2050: A vision of sustainable choices for a climate-friendly future’

38.

43.

55.

35. European Commission, ‘Communication from the Commission to the European Parliament, the council, the European Economic and Social Committee and the Committee of the Regions: New EU forest strategy for 2030’

3.

34.

22.

42.

19.

56.

Also to a number of technical experts from distributor members of EPTDA operating in this sector, who have provided the concrete examples included in the text and without whose contribution the document would lack its operational and commercial relevance and power for distributors.

31

32 WWW.EPTDA.ORG Copyright © 2022 EPTDA. All rights reserved. This work is registered with the IP Rights Office Copyright Registration Service Ref: 284745032